2011 News

Interesting articles regarding pension funds, state government and management.

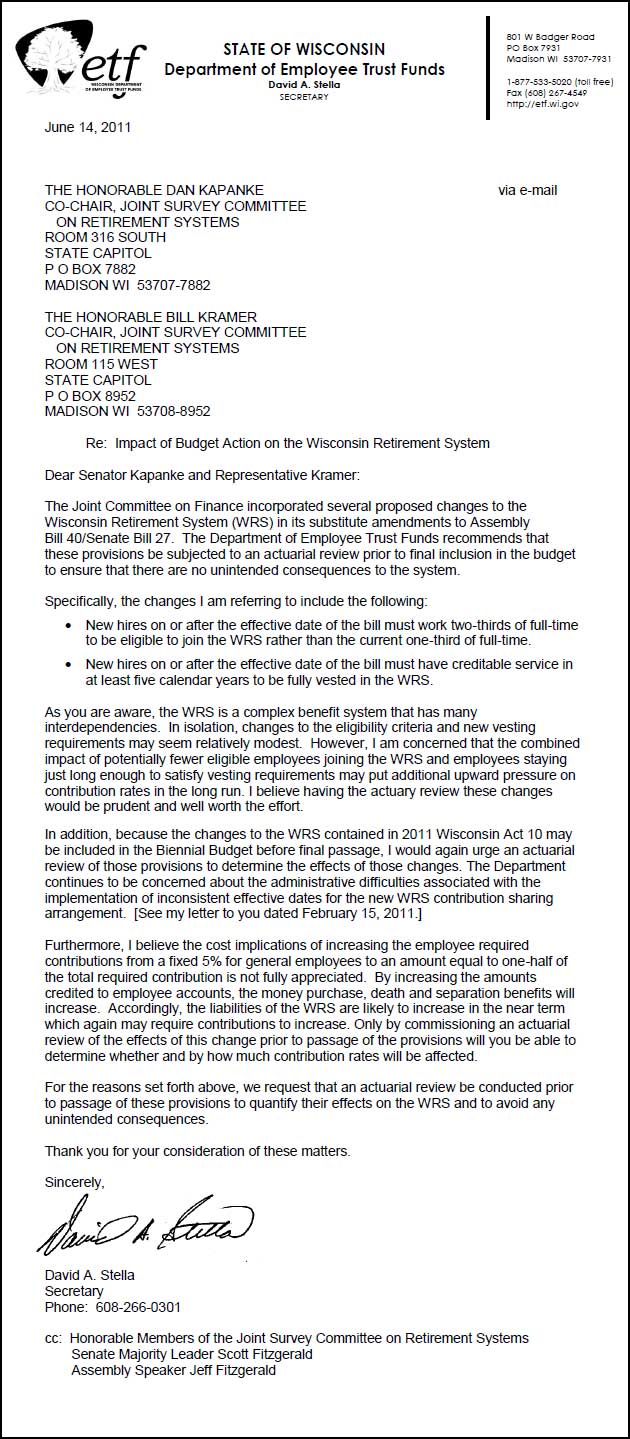

Note from Dave Stella, May 26, 2011

The following by Secretary Stella to the ETF staff, summarizes the JFC action that impacts ETF and it's future.

Good afternoon-

Many of you may be aware that the ETF budget was the subject of Joint Finance Committee action yesterday. I wanted to provide you an update on the actions the Committee took as soon as possible. JFC made decisions that impact our operations and our benefit programs more generally. A summary document (in Word) is attached that describes the actions in high-level detail. Also attached (the PDFs) are the most relevant motions and the Legislative Fiscal bureau paper that was the basis for many of the specifics regarding our agency budget.

In short, I am pleased that the Committee has been convinced of our need to build our capacity to meet the needs of our members. The budget action yesterday recommended new base funding and position authority, and left the door open to secure additional resources during this biennium for agency priorities. I have no doubt the reputation we have for excellent customer serviceespecially during recent monthshelped to convince the Joint Finance members that we are able stewards, and that we are facing unprecedented demand for our time and expertise.

The actions of the Committee have also charted a course for several changes to our benefit programs. The motion that passed yesterday would implement a vesting requirement for new employees in the WRS, significantly change the hours threshold to join the system from one third of full time to two thirds, and requires a number of studies on topics that could mean additional changes in the future. However, it is important to note that the study details did not include a mandate to evaluate any aspect of the accumulated sick leave credit conversion program.

The important thing to know about what Joint Finance did yesterday is that it is one step in the budget process. The bill still has to pass both houses of the legislature after the Committee finishes its work, and it must be signed into law by the Governor. While recent history is such that the bulk of Joint Finance recommendations ultimately make it to law, it is not necessarily always so. Its also the case that we have yet to see how these changes actually look in drafted form, so additional analysis is necessary. To that end, stay posted for further developments.

In closing, thanks for all you do. I appreciate it sincerely.

Dave Stella

Secretary, Wisconsin Department of Employee Trust Funds

Paper #290

Motion 308

VARIABLE FUND ELIMINATION

The following questions from an annuitant were answered by Secretary Stella.

1. With the variable choice cut-out and no new money coming in, no return to the variable once you opt out, and retirees in the variable dying, how can the variable fund be viable in the long run?

Answer: The Variable Fund will be viable for many years to come because funds will continue to be deposited from almost 70,000 current contributing members. Secondly, even as contributions decline the assets of the Variable Fund will continue to be very sizable. Many years in the future, as the fund balance gradually declines, a phase-out plan will need to be adopted. But that is many years away.

2 Why should you want to take the "big brother" approach in "protecting" some employees from themselves if they want to select the variable option clearly knowing the risk?

Answer:. A history of the Variable Fund creation is in order. When the Legislature created the Variable Fund in 1957 the WRS did not exist. There were three separate retirement systems that were all defined contribution plans. The assets of those systems were invested in a Fixed Fund that contained only fixed income (primarily bonds) assets. The Variable Fund was added to allow participants to create a balanced fund with up to 50% of their total contributions invested in stocks and the remainder in fixed income. The addition of the Variable Fund was based on the modern portfolio theory concept that advocated diversifying asset allocation to stocks and bonds to increase returns and reduce risk.

In 1965 the three retirement systems adopted a "defined benefit" plan based on a formula using credited service, the three high years of earnings and a formula factor. The defined contribution option that already was in existence was kept as a "money purchase" minimum option to ensure that members ' rights to that benefit form were preserved. The Variable Fund remained in place, but it had to be incorporated in the new defined benefit plan. This was done by a very complex process that resulted in Variable excess and deficiency calculations that were incorporated into the defined benefit structure. In the late 1970's the State of Wisconsin Investment Board, responding to the need to diversify the assets of the Fixed Fund began investing in stocks, real estate, alternative investments. Following the disastrous investment climate of the 1970's, WRS members in the Variable Fund demanded to be allowed to opt out of the Variable Fund. At that point they could not opt out. The Legislature and Governor enacted legislation allowing members to opt-out, but permanently closed the Variable Fund to new participants because the WRS was primarily a defined benefit plan. Substantially more assets in the Fixed Fund were invested in stocks and other asset classes which followed the higher prudent investor standard to diversify the investment of assets. For the next 20 years the Variable Fund remained closed to new members but grew larger with the unprecedented stock market run up over that period.

The Legislature passed WI Act 1999, which reopened the Variable Fund against the advice of ETF. One year later, after 65,000 new active members joined the Variable Fund the stock market declined for 3 straight years and the Variable Fund lost over 50% of its value. In addition, the Investment Board, by that time had invested up to 65% of the Fixed (Core) Fund in stocks, so participants in the Variable Fund were now allocating 85% of their contributions to stock, in combination with the Core Fund. While this might be appropriate asset allocation for a 20 year old, it clearly is not appropriate for participants in their 40's, 50's, 60's and 70's who are trying to create a stable retirement benefit. This resulted in a significant over-allocation to stocks and highly volatile returns for those in the Variable Fund. Use of the Variable Fund is no longer an asset diversifier as initially conceived in 1957. It has become impossible for members to protect themselves from market volatility with proper diversification as was witnessed in 2000-2002 and 2008. Participants are unable to "time" their way out of the Variable fund and as a result more and more Variable participants are facing the conundrum of "when do I get out of the Variable". In effect, Variable Fund members as a group ride a stock market waves up and down and are unable to effectively plan for stable, lifetime, retirement income. The Variable Fund no longer serves its intended purpose. It is important to remember that the purpose of the WRS is to provide stable, lifetime income to participants in the WRS. The Variable Fund was never intended to be a market speculation tool.

3. Are you rationalizing that because the returns for the Core and Variable have been about the same for about the same period of time, that it would be more cost effective to have only the Core to manage?

Answer: First, the returns of the Core and Variable have not been the same over time. The Core Fund, on average, has out-performed the Variable Fund since 1983. Second, the Core Fund is a fully diversified portfolio of assets and has an allocation to stocks that exceeds 50%. If you recall the original intent of the Variable Fund, which was to diversify assets into stock and fixed income assets, the Core Fund now meets the original purpose for which the Variable Fund was created. Further, the Core Fund has been made into an "all-weather" investment fund that better manages market volatility and market cycles. The State of Wisconsin Investment Board over the past several years has expressed concern about the Variable Fund's increasing volatility and it's lack of diversification. SWIB recommended that the ETF Board review the structure of the Variable Fund and recommended that it be closed. The ETF Board reviewed the concerns raised by SWIB and agreed with SWIB's assessment. The ETF Board then recommended that the Legislature enact legislation to close the Variable Fund to new participants because the ETF Board does not feel the Variable Fund meets the long-term retirement needs of WRS members.

4. Why should not an individual have the choice to feel the pain immediately, at certain times, in the variable rather than be anesthetized by "smoothing" of the Core?

Answer: This question assumes that the WRS provides mutual funds that allow individual members to speculate in equity markets by taking higher risk and thereby enhance their retirement benefit. In fact, that is not the intent of the WRS. The WRS exists to provide provide stable, lifetime income to its members at a reasonable cost to members and employers. S. 40.01 of the Wisconsin Statutes states that: "A public employee trust fund is created to aid public employees in protecting themselves and their beneficiaries against the financial hardships of old age, disability, death, illness and accident, thereby promoting economy and efficiency in public service by facilitating the attraction and retention of competent employees, by enhancing employee morale, by providing for the orderly and humane departure from service of employees no longer able to perform their duties effectively, by establishing equitable benefit standards throughout public employment, by achieving administrative expense savings and by facilitating transfer of personnel between public employers."

The history and purpose of the Variable Fund is not well understood. Further, the almost 20 year bull market cycle in the 1980's and 1990's caused WRS members to view the Variable Fund as " a way to take more risk and enhance their retirement benefit". The last 10 years have shown otherwise. About 25% of retired and active WRS members participate in the Variable Fund. The vast bulk of those members came in at stock market highs and now are inquiring about the "right time to get out". The vast majority of members are not invest experts and rely on SWIB to effectively manage the investment of Variable Fund assets and at the same time mange investment risk. SWIB has indicated that the Variable Fund cannot be effectively managed to meet both goals.

Dave Stella

Secretary, Wisconsin Department of Employee Trust Funds